Golden Mile - Sales Market Review 2024

Market Trends and Sold Prices in Golden Mile, Palm Jumeirah.

Author Gareth Davies - Award Winning Property Consultant and Broker

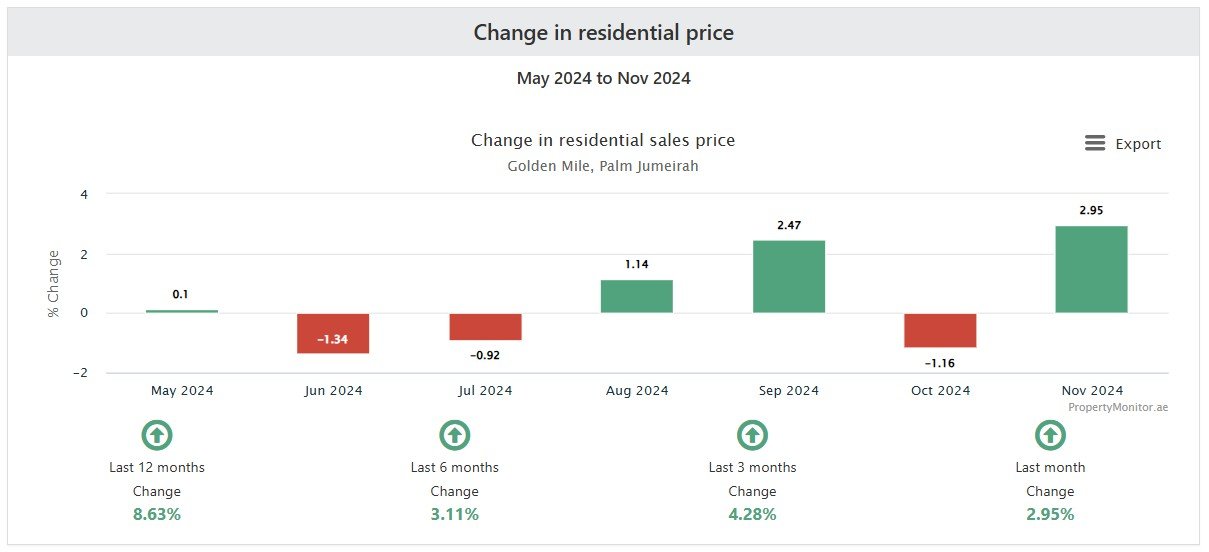

During 2024, the growth in the Sold Prices at Golden Mile (AED/sq.ft) has been slower than during 2023 and follows a similar trend in other communities in Palm Jumeirah. Although the volume of sales has decreased significantly since 2023, there is consistent demand from prospective buyers and the market activity still favours sellers.

Decline in Sales Volume in 2024.

Supply Constraints and Market Dynamics: The decrease in sales volume in 2024 can be attributed to a shortage of available vacant apartments and a shift in investor interest towards off-plan properties, where developers offered attractive payment plans. This shift diverted some demand away from the secondary market.

Data source: Property Monitor

Demand-Supply Imbalance:

The scarcity of vacant apartments caused a bottleneck in satisfying the demand of owner-occupiers and tenants transitioning into homeownership.

The mismatch between what buyers want and what is available likely suppressed transaction volumes despite ongoing demand.

Investor Reallocation:

Investors, once dominant in this segment, shifted to off-plan projects offering flexible payment plans, reducing their activity in Golden Mile's secondary market.

Price and Affordability Considerations:

The sustained increase in prices from 2022 through 2023 may have priced out some buyers or encouraged a wait-and-see approach.

Overall Five-Year Trend.

The Golden Mile market has evolved significantly:

Initially investor-driven, focusing on rental yields.

Post-2022, influenced by geopolitical factors and a shift towards owner-occupiers, pushing demand and prices higher.

By 2024, market activity slowed due to supply shortages and competition from off-plan developments.

Data source: Property Monitor

The market trends in Golden Mile, Palm Jumeirah, can be analyzed more comprehensively, accounting for both macroeconomic factors and changes in buyer behavior:

Key Factors Influencing Market Trends:

Investor-Dominated Market (2020–2021):

During this period, the majority of buyers were investors focused on yield potential. They were indifferent to whether apartments were leased or vacant, adjusting offers based on rental income or market rent potential.

This explains the strong growth in sales volume as investors capitalized on the recovering market post-COVID-19 disruptions.

Impact of the Russia-Ukraine Conflict (2022 Onward):

After February 2022, there was a noticeable shift in buyer demographics.

A surge in demand from Russian and Eastern European buyers who preferred vacant apartments for personal use (owner-occupiers) created significant upward pressure on prices and sales volumes in 2022 and 2023.

This demand likely drove record-high sales volumes during 2023, reflecting a market fueled by both new buyers and appreciation in property values.

Rising Rents and Tenant Purchases (2022–2024):

The sharp increase in rental rates from 2022 onwards incentivized many tenants to transition into homeownership to manage housing costs.

These buyers, also preferring vacant apartments, added further competition and price increases in the resale market, particularly in 2023.

Market Adjustment in 2024:

The decline in sales volume to 96 transactions in 2024 reflects several converging factors:

Supply Constraints: A lack of vacant apartments to meet the preference of owner-occupiers and tenant-buyers.

Shift in Investor Focus: Developers offering attractive off-plan payment plans diverted investor interest away from the resale market, reducing overall transaction activity.

Market Saturation: The rapid growth in prices and demand during the prior years may have temporarily exhausted a portion of the buyer pool.

Sold Prices from 2020 to 2024.

Golden Mile has seen a dramatic sales price growth since Q1 2020, increasing from AED 811 /sq.ft (AED 8,726 /sq.m) to AED 1,646 /sq.ft (AED 17,710 /sq.m) in Q3 of 2024 before a slight decrease to (AED 1,629 /sq.ft (17,528 /sq.m) in Q4 of 2024.

Data Source: Property Monitor

2024 Slowdown in the Rate of Growth.

The sustained increase in prices from 2022 through 2023 may have priced out some buyers or encouraged a wait-and-see approach.

While the decline in 2024 sales warrants monitoring, it does not undermine the overall growth trend.

Further analysis of market drivers (e.g., pricing, supply, or macroeconomic trends) is essential to determine whether this is a temporary adjustment or the start of a more prolonged slowdown.

The difference between average sold prices and average asking (list) prices provides valuable insights into market dynamics within a particular community.

1. Wide Difference (e.g., 85% of asking price):

Interpretation: The properties are selling at a significant discount compared to their listed prices.

Potential Reasons:

Overpricing: Sellers may have initially overestimated the market value of their properties.

Buyers’ Market: There may be an oversupply of properties, giving buyers more leverage to negotiate lower prices.

Market Weakness: Weak demand or unfavorable economic conditions may pressure sellers to reduce prices to close deals.

Distressed Sales: Sellers in financial distress might be willing to accept low offers to secure a quick sale.

Implications:

Suggests a lack of alignment between sellers' expectations and market reality.

Indicates a need for better pricing strategies to reflect true market value.

Buyers might perceive this market as offering opportunities for bargains.

2. Narrow Difference (e.g., 95% of asking price):

Interpretation: Properties are selling close to their listed prices, reflecting a strong correlation between sellers’ expectations and actual market value.

Potential Reasons:

Accurate Pricing: Sellers are listing properties based on realistic, data-driven market valuations.

Balanced Market: There’s a healthy equilibrium between supply and demand, with neither side having a distinct advantage.

Sellers’ Market: High demand or limited inventory might lead to less negotiation and more full-price offers.

Implications:

Suggests a mature and transparent market where pricing expectations are well-aligned with buyer behavior.

Encourages confidence in market stability for both buyers and sellers.

Sellers may have more pricing power, reducing the need to make significant concessions.

Summary.

A wide difference often signals a challenging market or pricing issues and might require sellers to adjust expectations or agents to focus on buyer education.

A narrow difference indicates a more predictable market where transactions happen efficiently, fostering confidence among stakeholders.

Understanding this difference is crucial for advising both buyers and sellers and tailoring marketing strategies effectively.

Concluding Remarks.

The market remains robust despite the 2024 slowdown, as the decline is supply-driven rather than a collapse in demand.

The decline in 2024 could indicate a normalization of demand following three years of rapid growth. This could also reflect cyclical market behavior or external economic pressures affecting buyer sentiment.

If you have questions and enquiries, kindly write to us via the form below or WhatsApp.

For more information please click on WhatsApp